Credit Card Chargeback Procedure

Have you ever opened your credit card statement and found a charge you didn’t recognize? Or worse, discovered that you’ve been a victim of credit card fraud? Don’t panic – in this article, we’ll show you how to dispute credit card charges and protect yourself from fraudulent activity.

takeaways:

- Check your statements regularly and dispute any fraudulent or incorrect charges.

- Understand different types of disputes and when to dispute charges.

- Know the chargeback process and be prepared to escalate disputes if necessary.

- Prevent credit card fraud by keeping information secure and monitoring credit reports.

- Try to resolve disputes with merchants directly before involving the credit card company.

- Keep records of communication and documentation related to disputes.

As credit card usage becomes increasingly common in our daily lives, it’s important to be aware of the potential risks that come with it. One such risk is the possibility of fraudulent charges on your credit card statement. In these situations, disputing the charges with your credit card company is crucial to protect yourself and your finances.

However, navigating the process of disputing credit card charges can often be overwhelming and confusing. From understanding the different types of disputes to knowing when and how to initiate a chargeback, there are many factors to consider. It’s important to know your rights and legal protections as a consumer, as well as how to prevent credit card fraud from happening in the first place.

In this article, we’ll provide a detailed guide on how to dispute credit card charges, with a focus on fraud prevention. We’ll break down the chargeback process and offer tips on how to effectively communicate with merchants. We’ll also provide resources for reporting suspected fraud and offer recommendations for keeping records and documentation.

Whether you’re a seasoned credit card user or just starting out, this article will provide valuable insights and information to help you navigate the confusing world of credit card disputes. So, let’s dive in and explore how to protect yourself from fraudulent charges on your credit card statement.

Understanding Credit Card Disputes

Credit card disputes can be a perplexing and frustrating experience for many consumers. Understanding what a credit card dispute is and the different types of disputes is crucial to successfully navigating the process. In this section, we’ll explore the ins and outs of credit card disputes and provide tips on how to protect yourself.

What is a Credit Card Dispute?

A credit card dispute occurs when a consumer contests a charge on their credit card statement. This can be due to a variety of reasons, including fraudulent charges, billing errors, or disputes with merchants over the quality of goods or services received. When a dispute is filed, the credit card company will investigate the claim and determine whether the charge should be reversed or not.

Types of Credit Card Disputes

There are several types of credit card disputes that consumers may encounter, including:

- Fraudulent Charges – These occur when someone uses your credit card without your authorization or knowledge. This can happen through a variety of means, including online hacking or physical theft of your credit card.

- Billing Errors – These can occur when a merchant charges you for the wrong amount, charges you twice for the same transaction, or charges you for a transaction that you didn’t make.

- Disputes with Merchants – These can occur when you have a disagreement with a merchant over the quality of goods or services received. For example, if you receive a product that is damaged or not as described, you may dispute the charge with your credit card company.

Legal Protections and Rights

As a consumer, it’s important to know your legal protections and rights when disputing credit card charges. The Fair Credit Billing Act (FCBA) provides specific guidelines for credit card companies to follow when investigating disputes. Under the FCBA, consumers have the right to:

- Dispute charges in writing within 60 days of the statement date

- Receive a response from the credit card company within 30 days of filing a dispute

- Have the disputed amount temporarily removed from their account during the investigation

- Be notified of the results of the investigation in writing

In addition to the FCBA, some credit card companies may offer additional protections and benefits for their cardholders, such as fraud protection or extended warranties on purchases.

Understanding credit card disputes and the different types of disputes is essential for protecting yourself as a consumer. Knowing your legal protections and rights can help you navigate the process more effectively and successfully resolve disputes. In the next section, we’ll discuss when to dispute credit card charges and offer tips on keeping records and documentation.

When to Dispute Credit Card Charges

VacationRentPayment

Knowing when to dispute a credit card charge can be a challenging decision for many consumers. In this section, we’ll provide guidance on when to dispute a charge and offer tips on how to keep records and documentation to support your claim.

When to Dispute a Credit Card Charge

There are several situations where it may be appropriate to dispute a credit card charge, including:

- Fraudulent Charges – If you notice charges on your credit card statement that you did not authorize, it’s important to dispute them immediately. This could indicate that your credit card information has been compromised, and prompt action can help prevent further fraudulent charges.

- Billing Errors – If you notice discrepancies in the amount charged or see a charge for a transaction that you did not make, it’s important to dispute the charge with your credit card company.

- Disputes with Merchants – If you have a disagreement with a merchant over the quality of goods or services received, it may be appropriate to dispute the charge. However, it’s important to try to resolve the issue with the merchant directly before filing a dispute with your credit card company.

Tips for Keeping Records and Documentation

When disputing a credit card charge, it’s important to have documentation to support your claim. Here are some tips for keeping records:

- Save Receipts – Always keep a copy of your receipt when making a purchase with your credit card. This can help provide evidence of the amount charged and the date of the transaction.

- Take Photos – If you receive a product that is damaged or not as described, take photos to document the issue. This can help support your claim if you need to dispute the charge.

- Keep Emails and Correspondence – If you have a dispute with a merchant, keep copies of any emails or correspondence related to the issue. This can help provide evidence of your attempts to resolve the issue directly with the merchant.

- Review Your Statements Regularly – It’s important to review your credit card statements regularly to identify any unauthorized charges or billing errors as soon as possible.

In conclusion, knowing when to dispute a credit card charge and how to keep records and documentation can help you successfully navigate the dispute process. Remember to always try to resolve issues with merchants directly before filing a dispute with your credit card company, and keep detailed records to support your claim. In the next section, we’ll discuss how to initiate a chargeback and the process for disputing a credit card charge.

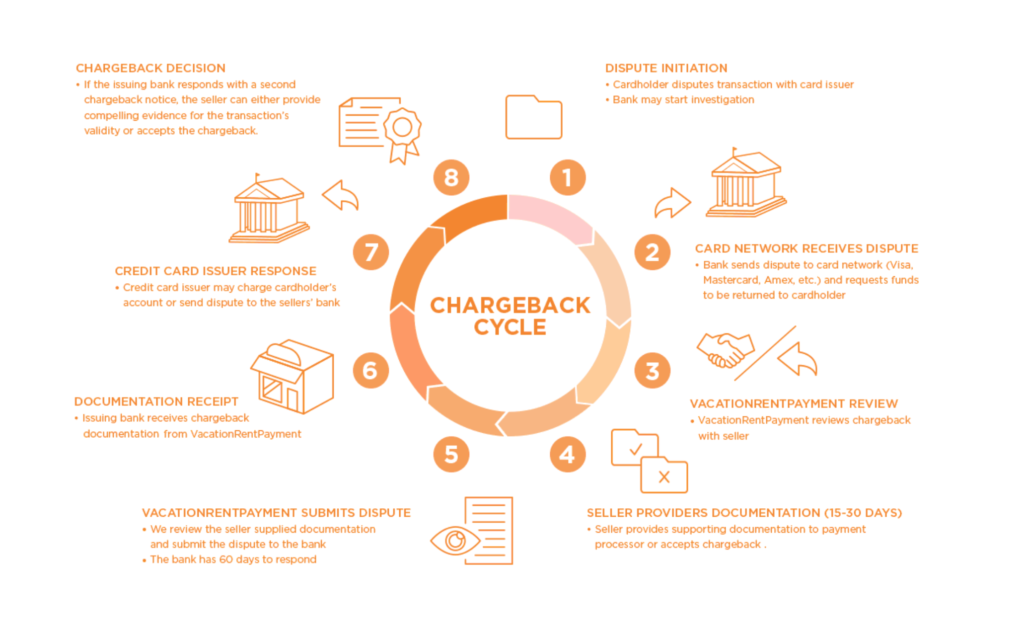

The Credit Card Chargeback Process

If you’ve determined that disputing a credit card charge is necessary, the next step is to initiate a chargeback with your credit card company. In this section, we’ll provide an overview of the chargeback process and offer tips on how to maximize your chances of a successful outcome.

What is a Chargeback?

A chargeback is a dispute process where a credit card company reverses a transaction and returns the funds to the cardholder. The chargeback process is governed by federal law and provides protections for consumers who have been charged for goods or services that were not received or were defective in some way.

How to Initiate a Chargeback

To initiate a chargeback, you’ll need to contact your credit card company and provide them with the details of the disputed charge. This typically involves filling out a form and submitting any supporting documentation that you have, such as receipts, emails, or photos.

The credit card company will then review the dispute and may request additional information from you or the merchant. If the credit card company determines that the dispute is valid, they will reverse the transaction and credit the funds back to your account. If the credit card company determines that the dispute is not valid, they will notify you of their decision.

Tips for Maximizing Your Chances of a Successful Outcome

To increase your chances of a successful chargeback, there are a few things you can do:

- Act Quickly – It’s important to initiate a chargeback as soon as possible after noticing a disputed charge. Delaying can make it harder to gather evidence and may limit your ability to dispute the charge.

- Provide Detailed Information – When filling out the chargeback form, provide as much detail as possible about the disputed charge, including the date of the transaction, the amount charged, and any supporting documentation you have.

- Be Persistent – If your initial chargeback is denied, don’t give up. You may be able to provide additional evidence or appeal the decision to a higher authority.

- Consider Seeking Legal Advice – If the dispute involves a significant amount of money or legal issues, it may be helpful to consult with a lawyer who specializes in credit card disputes.

Preventing Credit Card Fraud

One of the best ways to avoid the hassle and stress of disputing credit card charges is to prevent fraud from happening in the first place. In this section, we’ll provide tips and best practices for preventing credit card fraud.

What is Credit Card Fraud?

Credit card fraud is any unauthorized use of a credit card or card information to make fraudulent purchases or withdrawals. Credit card fraud can take many forms, including skimming, phishing, and hacking.

Tips for Preventing Credit Card Fraud

There are several steps you can take to reduce your risk of falling victim to credit card fraud:

- Check Your Statements Regularly – Reviewing your credit card statements regularly can help you identify any fraudulent charges quickly. If you notice any unauthorized charges, report them to your credit card company immediately.

- Use Secure Websites – When making online purchases, only use secure websites that have an “https” in the URL and a lock icon in the address bar. This indicates that the website uses encryption to protect your information.

- Don’t Share Your Card Information – Never give out your credit card information over the phone or via email unless you’re certain it’s a legitimate request. Legitimate companies will never ask for your credit card information via email.

- Be Careful With Your Card – Keep your credit card in a secure location and don’t let others use it. If you lose your card, report it to your credit card company immediately.

- Use Two-Factor Authentication – Many credit card companies offer two-factor authentication, which requires a second form of identification, such as a text message or a fingerprint scan, to verify your identity. This can add an extra layer of security to your account.

- Monitor Your Credit Report – Monitoring your credit report regularly can help you identify any suspicious activity, such as new accounts or credit inquiries that you didn’t initiate.

By following these tips and being vigilant about protecting your credit card information, you can reduce your risk of falling victim to credit card fraud. However, if you do become a victim of fraud, it’s important to take action quickly to limit the damage and prevent further fraudulent activity.

Resolving Disputes with Merchants

Sometimes, credit card disputes can arise due to a misunderstanding or mistake on the part of the merchant. If you believe that you have been overcharged, received defective merchandise, or didn’t receive the product or service you were promised, you can try to resolve the dispute directly with the merchant.

Here are some tips for resolving disputes with merchants:

- Contact the Merchant – The first step is to contact the merchant directly and explain the situation. Be polite but firm and explain your side of the story. Try to reach a compromise or resolution that satisfies both parties.

- Keep Records – Keep records of all communication with the merchant, including phone calls, emails, and any documentation related to the dispute. This will be helpful if you need to escalate the issue to your credit card company.

- Be Persistent – If the merchant is unresponsive or uncooperative, don’t give up. Be persistent and keep pushing for a resolution.

- Know Your Rights – Familiarize yourself with your rights as a consumer. Many states have consumer protection laws that can be helpful in resolving disputes.

- Escalate the Issue – If you are unable to resolve the dispute directly with the merchant, you can escalate the issue to your credit card company. Be sure to provide all documentation and records related to the dispute.

It’s important to note that disputing charges with a merchant can be time-consuming and frustrating, and there’s no guarantee of a satisfactory resolution. However, it’s always worth trying to resolve the issue directly with the merchant before escalating the dispute to your credit card company.

As we’ve discussed in this article, disputing credit card charges can be a complex and frustrating process. However, with a little persistence and knowledge of the process, you can protect yourself from fraudulent charges and resolve legitimate disputes with merchants.

Remember, the first step is always to review your credit card statement carefully and identify any charges that you don’t recognize or that seem suspicious. If you believe that a charge is fraudulent or incorrect, don’t hesitate to dispute it with your credit card company.

In many cases, the credit card company will be able to resolve the dispute quickly and efficiently. However, if the issue is more complicated, you may need to initiate a chargeback and escalate the issue to a higher level.

It’s important to keep in mind that credit card disputes can be time-consuming and frustrating, and there’s no guarantee of a satisfactory resolution. However, by being persistent and informed, you can protect yourself from fraudulent charges and ensure that you’re only paying for legitimate purchases.

If you have any further questions or concerns about credit card disputes, be sure to consult with your credit card company or a financial advisor. With the right knowledge and preparation, you can protect yourself from credit card fraud and resolve disputes quickly and effectively.